No reward for taking on small loans with lots of “headaches”

|

NAR study shows, after tax incentive expired, first time

homeownership plunged. (NAR 2014)

|

Originator Compensation Caps - Another Example of Price Control Failure

Basic economic principles dictate that price controls distort markets and create disincentives. When the Carter administration implemented price controls on consumer goods in an attempt to mitigate the effects of inflation, the supplies of milk predictably dried up. When New York City implemented rent controls to limit the rate of rent growth, the supply of existing rental housing constricted. This same principle goes into effect when the maximum fee on a mortgage loan doesn't cover the structural costs of production.

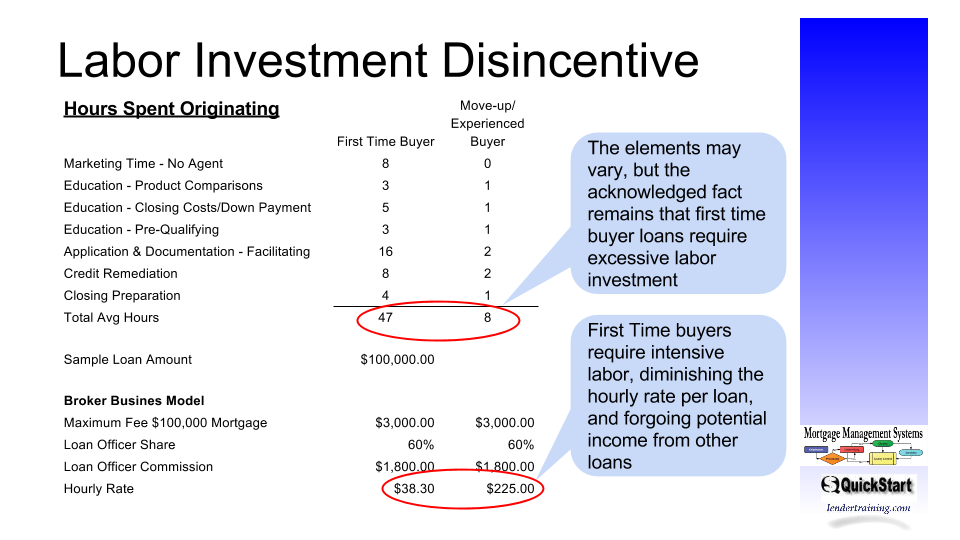

Fair Hourly Wage Comparison - Originator Compensation

While many mortgage loan originators strive to earn six figure incomes, earnings at that level normally accrue only to top producers or those fortunate enough to originate in areas of high loan balances. According to the Bureau of Labor Statistics, the 2012 Median Pay for mortgage loan officer was $59,820 per year or $28.76 per hour. Loan officers normally receive commissions, not a salary, so they make business decisions about how to maximize the value of their time. First time home buyers require much more work than move-up/experienced borrowers.

|

| Figure 1: This shows the amount of time a loan officer spends to originate a first time buyer loan compared to the time spent working with an experienced borrower. Even if the hours get attributed differently, no loan officer would argue that a first time borrower is LESS work. |

Due to the extra number of hours spent sourcing and processing loans to entry-level or first time borrowers, loan officers have an incentive to avoid these loans and focus on larger loans to more sophisticated and well-qualified borrowers. Figure 1 reflects the rationale for avoiding loans to first time buyers. The reward is comparatively low for the amount of work.

The fixed cost nature of the mortgage business makes these loans unprofitable for mortgage brokerage companies, but particularly for mortgage lenders whose fixed infrastructure costs and compliance costs tend to be much higher. Figure 2 shows that for a $100,000 loan, with a 3% fee structure, these loans actually lose money for the firms. (Per loan cost basis varies dependent on loan volumes - higher loan volumes bring per loan costs down, but low volumes drive per loan cost up.)

.png) |

Figure 2: Commission income and loan profitability for small loans decreases markedly. Cost source: Broker - cost Analysis; Lender (Finklestein 2014)

|

The current regulatory system creates massive disincentive for loan originators who work for lenders, because their compensation cannot vary as a result of loan features. In Figure 2, a loan originator who makes an industry standard commission of 60 basis points, working on a ends up with an hourly compensation rate of $12 an hour on small loans for first time buyers. This, by itself, can explain the structural problems related to stimulating the housing market.

The inflexibility created by Loan Originator Compensation Rule and Anti-Steering Rules, prevents lenders and brokers from adjusting loan pricing to offset the cost of making small loans. These rules impact the compensation of loan officers who work for lenders even more dramatically than brokers, so when you add the higher time investment required for first time buyers, loan officers working for lenders have the greatest disincentive to make these loans. Lenders account for 89% of all mortgage production (Bancroft 2014)

HPML Impact on Small Loans Aggravates Supply Constriction

The Higher Priced Mortgage Loan (HPML) Rule further restricts loans that exceed rate thresholds by increasing lender liability, documentation requirements, scrutiny of appraisals, and limiting the flexibility of underwriting. Many loans with small down payments already trigger the HPML thresholds by virtue of the mortgage insurance costs. The rule's thresholds further limit the fees that a lender can charge to offset the cost of originating smaller loans.

Conclusion - Eliminating Price Controls May Represent Only Solution

|

Figure 3: While the percentage of buyers purchasing new

homes has declined, the percentage of buyers purchasing

new homes has increased. This shows builders have adapted

to the new environment.

|

Examining several examples of home builders who specialize in building product for the first time buyer shows they have developed their lending systems to specifically accommodate this model, and rationalize the loan production losses with the profits on the home sale. Figure 3 shows how the the creativity and natural balance in a market where businesses innovate to overcome problems. Builders can focus on a particular segment and design a business model that meets a particular need. However, the market as a whole cannot overcome a set of regulatory rules designed to affect the entire market.

This ironic situation, where the regulatory structure actually hurts the population it intended to protect, hurts the markets which need financing the most. The real estate markets which have failed to recover from the 2008 crash exhibit a large percentage of loans impacted by this effect. The constriction on financing exacerbates the slowness of the recovery.

While the issue requires further data analysis, common sense supports this hypothesis. Only loan fee de-regulation will reverse the declining share of first time buyers in the market. Without this, the housing market's regulatory structural defect will prevent any broad, long term resurgence in real estate.

Author: Thomas Morgan

Citations

Bancroft, John. Mortgage Brokers Gained Market Share in Second Quarter, At Least on GSE Loans. Inside Mortgage Finance. July 10, 2014

Berndt, Antje, Hollifield, Burton and Sand, Patrik. What Broker Charges Reveal about Mortgage Credit Risk, SEC http://www.sec.gov/divisions/riskfin/seminar/berndt091312.pdf. June 2012

Finklestein, Brad. Companies began to increase compliance staff to deal with the new rules and that helped to increase the net cost to originate to $5,171 per loan in the fourth quarter from $4,573 in the third quarter. National Mortgage News, April 2014.

Lautz, Jessica. 2014 Profile of Buyers and Sellers. National Association of REALTORS®, October 30, 2014

National Association of Homebuilders, Housing Market Survey 2012

I have had so much response to this topic. Everyone agrees this is a problem. One LO wrote

ReplyDelete"This is a tough problem. It is a struggle to justify the huge amount of work involved when the reward is so low. The problem is nobody makes any money on the "small" loans but they take as much if not more work to get to closing. You want to help everyone you can and of course you can't discriminate due to amount."

Mr. Mel Watt, Director of the FHFA spoke at the NAR Convention, parrots the same tired explanation for why entry level buyers people aren't buying. Student loan debt, preferring to rent, saving for down-payment, and constricted underwriting all make their appearance as the standard explanations. But none of these are more true today than in the 80's, 90's or pre-meltdown 00's. So what's the explanation? Price controls instituted by the over-reach of the CFPB in drafting the rules required by Dodd-Frank.

ReplyDeleteDodd-Frank NEVER said "limit compensation" or "limit fees charged", but the CFPB undertook the idea of compensation: "how much is a fair price for a service" out of the hands of the market. Now they are reaping the effects of that policy.

http://www.fhfa.gov//Media/PublicAffairs/Pages/Prepared-Remarks-of-Melvin-L-Watt-2014-NAR-Conference.aspx

All this stuff is pretty obvious to anyone with a rudimentary level of economics. Unfortunately, we have a political party that doesn't understand business and how markets work. Regulation almost always increases prices, stifles productivity, and hurts the very people it is supposed to be helping.

ReplyDeleteIf it were any more apparent, here is an article from one of the top sales gurus in the industry saying "focus on the big loans!" to make more money.

ReplyDeletehttp://www.nationalmortgagenews.com/news/commentary/doing-less-work-getting-paid-more-1043097-1.html?utm_campaign=daily%20briefing-nov%2010%202014&utm_medium=email&utm_source=newsletter&ET=nationalmortgage%3Ae3320003%3A31104a%3A&st=email

LOs Need to Meet the Needs of All Millennials

ReplyDeleteby BRAD FINKELSTEIN

In loan officers' efforts to show they can meet the needs of one set of millennials, they shouldn't forget about the other buyers that can be helped.

Brad - Unfortunately, it's not the millenials, as everyone keeps saying. It's the fact that no one wants to spend the amount of time it takes to walk a first timer through the process for the paltry reward.