Many brokers and mini-correspondents spend unnecessary money and time on QC Audits that aren't required

How to Use Checklists and Investor Underwriting to Implement Your QC Plan

The problem becomes more pronounced when brokers transition to mini-correspondent or non-delegated lender status. Lending partners, investors and other providers apply the same requirements for these transitional business models as they do for fully delegated mortgage bankers. The result: Your scope for auditing loans includes auditing the lending partner's work. The ultimate lender holds the responsibility for conducting these audits, which doesn't mean that non-delegated correspondents don't conduct audits, but need to limit the scope of audits to the work actually performed.

The question is: What is the scope of the non-delegated correspondent/lender's audit? That depends on the roles the institution performs, not the name or industry moniker. You must take care in explaining these roles, as part of the confusion comes from the fact that table-funders like to represent themselves as lenders to the public; it connotes a greater sense of institutional fortitude. However, when this representation carries into its dealings with lending partners, the lender label adds those unnecessary functions.

Understanding Which Functions Require Audit

|

| Image 1 - Lenders carry additional audit responsibilities if they take on actual underwriting and closing functions, and those are not performed by proxy, such as delegated closing agents, or any pre-funding underwrite. |

|

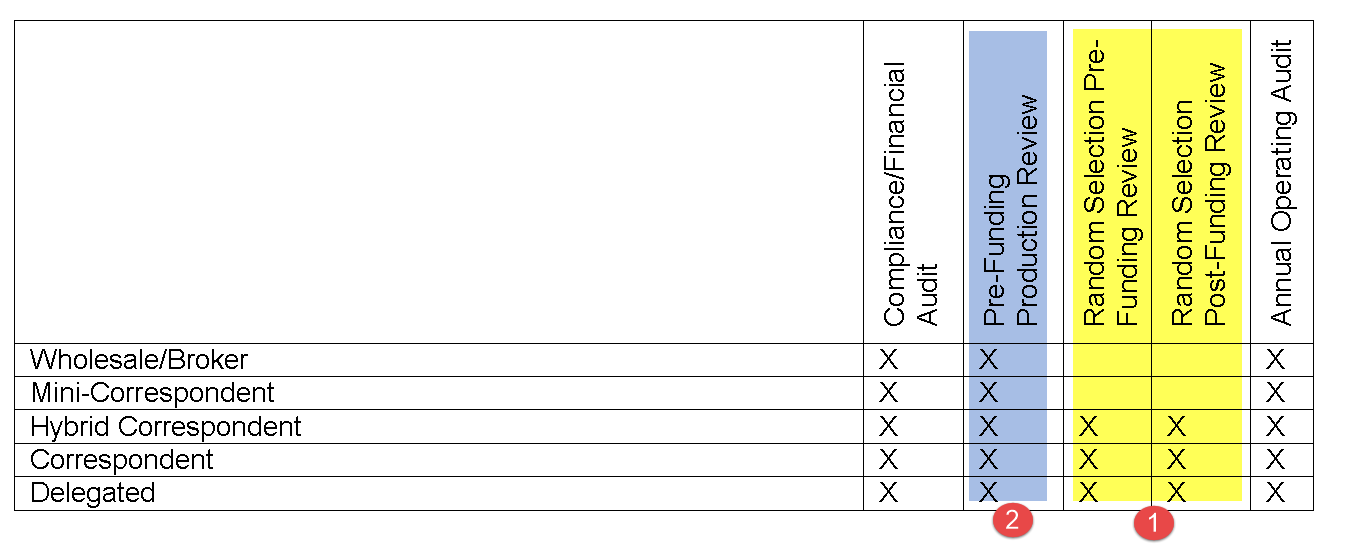

| Image 2- 1.) Delegated Lenders perform random selection reviews on a percentage of all production. 2.) Everyone must conduct pre-funding reviews, and lender reviews of a non-delegated |

Delegated Lenders conduct Post-Closing Random Audits - Non-Delegated Do Not!

How to Create Quality Control Reports Without Using a Third Party Auditor

Checklists are foundational quality control elements and can improve process efficiency and identify problem areas. But bad checklist practices can create more problems than they potentially solve.

If you have spent any time in the industry, you have seen checklists of one fashion or another. In mortgage banking, where there are literally 3,000 quality control checks in a single loan file, it's hard to conceive how any individual - new initiate or seasoned pro - could keep all of the elements in mind while reviewing a loan file. So, naturally, some sort of job aid evolves in every workplace. We need to applaud those who develop these tools because they have so many overlapping beneficial purposes and uses. But while even a bad checklist or form can solve some problems, companies don't realize their full benefits unless they use one designed to capture all purposes and work within the flow of a particular function's duties.

Independence - At the Core of Auditing

The insistence on independence in the review process comes from the idea that 1.) you are too close to your own work to review it and 2.) you are pre-disposed to cover up any errors you make, so these preclude you from auditing your own work. However, if honestly adhered to, checklists can create independence. Checklists don't fudge reports, or have a bad day and miss things they ordinarily wouldn't. So you don't have to hire a 3rd party auditor to obtain independence. You just need a good checklist.

Consistency

By using a single checklist across your platform, many of the misunderstandings and inefficiencies get eliminated because everyone works through the same form. No surprises!

Checklist Design Best Practices

In designing a checklist, think about the process or documents you use the checklist to review. Key principles in this process

- You may use the review data again; more than just as a checklist for a processor, for example. You need a format that you can easily break up and re-integrate. Although you can get nicer formatting through Word, you can more easily access and manipulate data in Excel. A worksheet that will be used as a training tool, that contains manual calculations, or handwritten notes for one time use, lends itself to Word formatting. An audit checklist, which you use for extracting missing or erroneous items from a long list, lends itself to Excel formatting, so you can export the information into your LOS or aggregate into reports.

- You can use prompts within the descriptive fields as a decision tree. For example If>then statements, or by identifying specific guideline triggers such as $____ > $, then... This level of detail allows you to aggregate the descriptive information in any report. This is one of those areas where you can get more bang for your buck from the process by understanding the different ways you can use the information garnered through the checklist review.

- Organize the form in a way that a reviewer would rationally progress through the file. For instance, in a cross check of property address, rather than having the reviewer stop and browse through application, contract, W-2 and paystub, appraisal, survey and any other address bearing exhibit, review each exhibit one time, coming back to confirm information. Awkward checklists that make the user bounce around the file or the form don't get used and create more mistakes than errors they solve.

- MAKE SURE BINARY CHOICES ALWAYS ADDRESS THE SAME POSITIVE OR NEGATIVE CONTEXT!! One of the most common faux pas on a checklist is having a yes/no box, but the yes or no have different meanings. This makes the reviewer have to review the entire checklist item again when recording findings. Phrase checklist elements to only flag a check if an item is wrong, or for a no flag to indicate non-compliance. For instance, don't have one question saying "is the earnest money deposit check cleared?" which a yes would be a non-finding; the next question shouldn't be "is there any evidence that the property is not owner occupied?" where no is a non finding.

- COMPRESS! While this can be taken to extremes (I have been guilty of this; trying to get it all on ONE PAGE!), do pay some attention to not making forms excessively long. AT A MINIMUM, on a multi-page form, try to insert page breaks when the context or content changes; again, keeping the reviewer from bouncing between pages. (The one at left turns into a 10 page pre-funding review because of white space and inattention to compression.)

- WHITE SPACE can be useful, but having white space simply because of a long descriptor makes for a very long form. This is the kind of thing the government would do.

- Multiple versions of the same checklist. We often see multiple varieties of a single checklist used for different types of loans. This multiplies the likelihood that a checklist won't get updated when there is an across the board change. Most frequently this appears in underwriting checklists, but elsewhere as well, when you have a different checklist for FHA/VA/Jumbo Investor/MI and other specs which vary slightly. In cases where the bulk of the checklist (up to 50% or more) consists of items reviewed on every loan, you shouldn't create separate versions of checklists in this way, but should work to create dropdown lists which highlight the specific investor guidelines.

Adding This Information to your LOS to Create Your QC Report

Most LOS' have the ability to record "conditions" or other items stipulated by the underwriter. A common error we see involves the individual taking the conditions resulting from an underwriting or closing prep review and typing them into a separate e-mail to the customer or other party for assistance in resolving. You have accomplished one goal - communicating the information to the customer - but you have no record of that.

Step 1: Record the Data in the LOS

Instead of this two-step process, record the conditions in the LOS and use that data to generate a customer notification. Then, as the documents come in, mark the date received and the date satisfied. This forms the foundation of the quality control report.

Step 2: Identify Items as Critical/Clerical/Compliance

Critical items include things that could potentially cause the loan not to close. These items get referred to as "suspense" items, potential fraud, or general mis-qualification. These critical defects should have a target rate of "0".

Clerical items include missing documents, errors that require explanation or correction, and checklist items not critical to loan approval, but that complete the documentation requirement

Compliance items could potentially cause the loan not to close. These compliance items can reveal repetitive system error.

Step 3: Evaluate your Defect Rate

Your defect rate has two components. Gross defects include the total number of defects in each category. Net defects reflect the number of defects AFTER you have made all corrections or resolved each issue.

Once you start collecting data, you will start to see the trends, and can identify an average defect rate for each category. Without making any adjustments to your system, you will use this average defect rate as your target defect rate. However, if you recognize that your Gross Defects are too high, you can initiate a correction in your process, and then compare your defect rates month over month to determine whether any changes you made to process. In addition, these numbers become your quality control report, whether monthly, quarterly or annually.

No comments:

Post a Comment