As we get into a more competitive real estate environment, where all-cash offers aren't the only way for a buyer to make an offer that might be accepted by a seller, these questions surface again. Specifically, how much about a customer can we share with a listing or selling agent?

Understanding Real Estate Agent's Role

First, understand that real estate agents, for the most part, have a fiduciary responsibility to the seller. While selling agents (who work with buyers) say they work for the buyer - and may even have the buyer brokerage disclosure or contract signed - the real estate agent is paid by the seller. So information about a customer's profile, the likelihood of getting financing, and other transactional information a loan originator may possess can be pretty valuable to a seller.

Loan originators often pass this information out to the agent who referred them to the transaction as a way of currying favor with the agent. You must carefully monitor and limit this data flow for many reasons. For example

- While negotiating a contract, a seller wants to obtain the highest price and net proceeds. The buyer wants the opposite. If a loan originator offers a prequalification or pre-approval letter, the seller wants to know if the buyer can afford more. The loan originator capitulates and says, "well, he can afford another $200,000 in the loan amount," the seller may counter-offer a higher amount. The buyer, however, asked for prequalification for a certain amount, and the originator's disclosure took away the buyer's leverage.

- While processing a transaction, the seller accepts backup contracts, perhaps more favorable than the current contract. With the information that financing is still pending or in question, the seller may act in ways that further diminish the buyer's ability to consummate the transaction to obtain a more favorable sale.

- The loan is denied, and the seller wants to know "why?" The seller is trying to figure out if the borrower did something wrong - acted in bad faith, perpetrated fraud, or another scheme - that kept the property off the market during the financing contingency period. The seller wants to keep the buyer's deposit because they needed to actively pursue financing.

Pre-Qualification is NOT an Approval; it's an Opinion

A buyer asks for your opinion on how much he or she can afford by asking to be prequalified. You should address that pre-qualification letter, certificate, or other documents to the prospect, not the real estate agent. Then, if the real estate agent has questions about the customer's qualifications, such as where is the money for the down payment coming from, what their monthly debts are, how they receive their income, etc., the agent should address it to the prospect.

Prospects should be careful about what information they provide to a real estate agent because they risk exposing their Personally Identifiable Information or their Non-Public Information to identity thieves. Real estate firms generally are not regulated by entities that insist on secure data because most real estate-specific information is public knowledge.

On the other hand, the agent will likely communicate the information to the seller in support of an offer to purchase, so a prospect may feel compelled to share more information than prudent to advance their home purchase.

To avoid disclosing this information, a prospect should actually obtain the financing in question via a loan application, loan underwriting, and loan commitment, subject to a final property selection; a pre-approval. With this in hand, the customer does not have to provide additional documentation supporting an offer contingent on financing because the financing has already been obtained.

How Much Can You Share?

Technically, none. Your customer has a right to limit the information you share and under what circumstances the information is shared. To share any information a prospect gives you, you should review a copy of the sales contract (offer) to see if the customer has already authorized the lender to share information on loan status. Otherwise, you should obtain authorization to release information to the agent(s) or builders; Consent to deliver loan status updates, generally.

Loan Status vs. Personally Identifiable Information or Non-Public Information

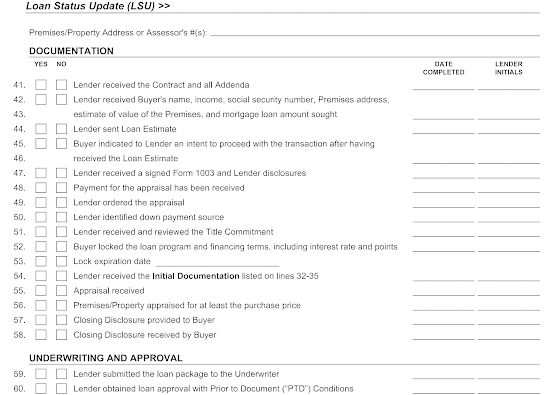

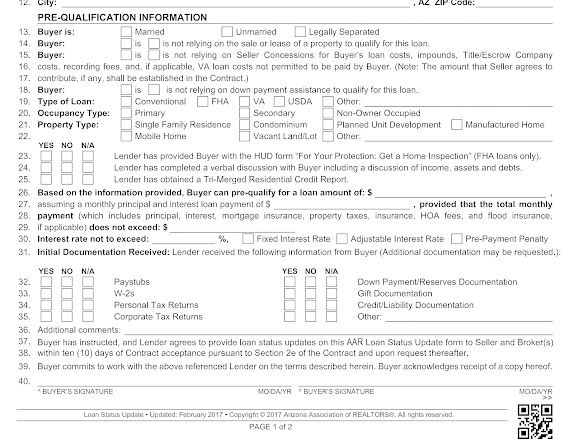

Loan status simply details what is in and out on a loan file and provides dates when certain tasks have been performed on a transaction. This is a good example of how this information could be shared (Source: AZ Association of Realtors). There is no NPI or PII in any of this material.

When the loan originator provides Non-Public Information or Personal Financial Information, such as credit scores, payment history, or any other information gathered during transacting business or in conjunction with a loan application, this is a clear violation of the Gramm-Leach-Bliley Privacy Act. It MAY be permissible in a situation where there is an affiliated business and the sharing of information would be NECESSARY to conduct business.

So, NO. Don't Share Private Information

In other words, a customer may share their own information, but you, as a financial service provider, may not provide any non-public private information.