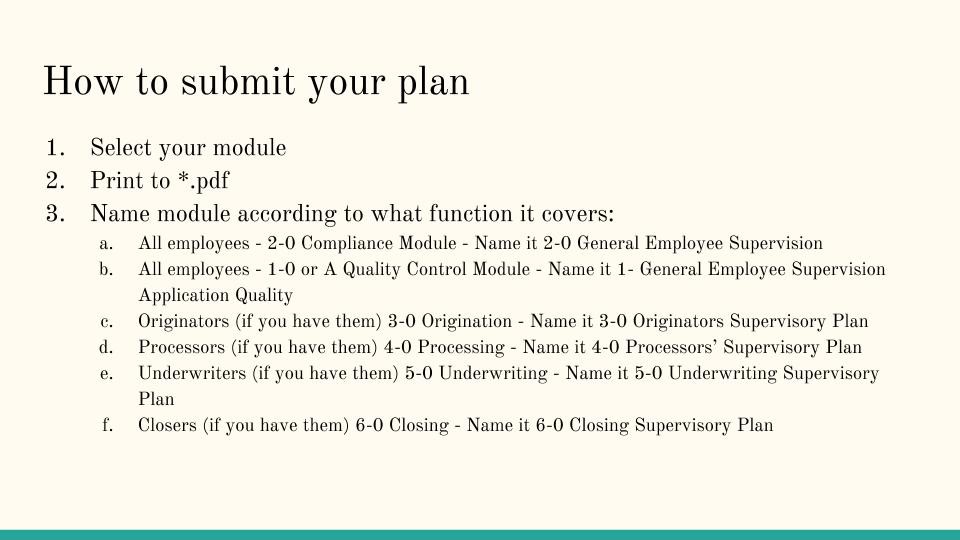

Vague Company Licensing Requirements can Cause Confusion

With the surge in the mortgage demand, we see many new companies throwing their hat in the ring to become a licensed provider. For the uninitiated, prepare to spend some time gathering and uploading documents. For new and experienced alike, some of the requirements, and the vague way the Nationwide Mortgage Licensing System describes them in their requirement templates, can cause confusion. We get many of these calls every day. Here we provide a primer on answering the less obvious requests:

Provide a Copy of Your Business Plan...

A business plan is a great idea. The SBA definition of a business plan, and what most people think of as a business plan - including agencies like Fannie/Freddie and others - allows you to memorialize how you will do business; the ways and means including LOS selection, pricing, startup costs, volume projections, staffing as well as unique business propositions, marketing strategies, and other relevant elements. It looks like this:

This is a sample of a table of contents of an SBA-Style Business Plan

But... THIS IS NOT what the regulator wants. The regulator wants an answer to specific questions about how you will do business. We recommend that you write a 1 pager and simply answer the questions in a Q&A format. In this way, there can be no question as to the narrative. For Example:

NMLS Requirement for a Business Plan which is quite vague

For the business plan requirement, we recommend that you simply draft a memorandum answering the questions:

- What is your marketing strategy?

- What products will you offer?

- Who will you market these products to?

- How will you operate - e.g.; branch processing, centralized? Manager? Loan Originators? Processors? Whom will they report to?

Organizational Chart Requirement

Once again, an organizational chart makes a great tool to ensure that all of a company's responsibilities get assigned to an individual and who reports to whom. Microsoft includes a good organizational chart template in Word, which we use in our products, too, as below.

Sample Organizational Chart for a Mortgage Business

However, for a small company, an organization "Chart" where you draw lines between functions doesn't really apply.

This is the text from the NMLS requirement for an Organizational Chart

Again, instead of a policy, draft a memorandum to Identify who, within your organization, is in charge of:

- Compliance - reports to?

- Production Sales - reports to?

- Processing, Operations - reports to?

- Financial Control - reports to?

If these are all the same person, then state that.

If you have any questions about licensing, or if you just want to hand it off to someone else to manage, please let me know.

MortgageManuals.com does include the business plan in the Complete Broker, Correspondent, Lender and Compliance Packages.

#mortgagelicensing #mortgagecompliance #mortgagebroker